As lending standards have loosened over the past four years, closing rates have steadily improved and in August, approvals rates for all mortgages were more than 50 percent higher than they were in August 2012, according to the latest Origination Insights report from Ellie Mae.

Closing rates increased from less than half of applications—47.8 percent in 2014—to 72.3 percent of applications in August 2016. Approval rates on purchase loans did not rise as much, but reached a new historic high, rising from 60.1 percent of applications to 76.6 percent.

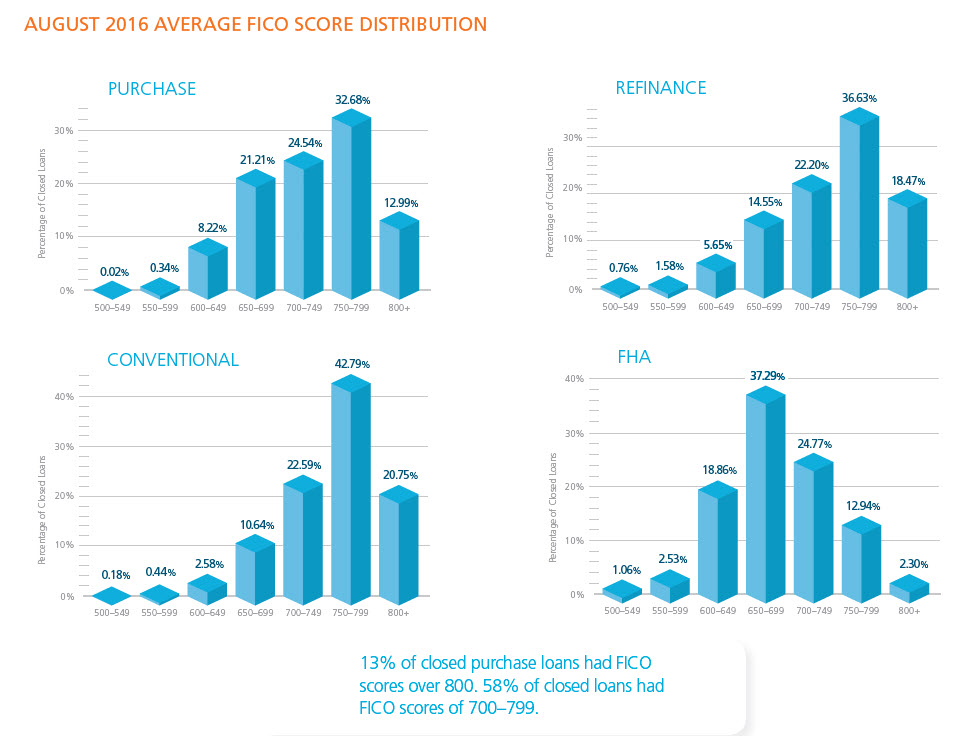

The dramatic turnaround in loan approvals reflects changes in lending standards, which tightened dramatically following the subprime crash in 2007 but loosened over the past decade. Since 2012, average FICOs for all loans have fallen from 750 to 731. Loan to value ratios are about the same: 80 percent in 2012 and 79 percent in 2016. Debt to income ratios are also more forgiving today, rising to 14/36 from 23/35 in 2012 despite the enactment of the QM rule last year. To qualify a mortgage under the new rule, most lenders will not approve a back end debt to income ratio higher than 43 percent.

However, looser standards may not be the only reason closing rates have improved. Buyers, especially first-time buyers, may be better prepared for the process of obtaining a mortgage today than they were in 2014. The percentage of first-time buyers who said they had to make sacrifices to save for a down payment fell from 42 percent in 2012 to 30 percent in 2015. However, the percentage of first-time buyers who found the mortgage application and approval process to be more difficult than they expected increased slightly, from 32 percent in 2014 to 35 percent in 2015, according to the National Association of Realtors’ Profile of Home Buyers and Sellers. The 2016 version of the NAR report will be released in November.

Source: Ellie Mae Origination Insights Report, August 2016

Related Posts

Justin Verlander and Kate Upton are selling their Benedict Canyon estate

Justin Verlander and Kate Upton are selling their Benedict Canyon estateHere's why closing the sale of a condo has suddenly become harder for an association

Use Plants to Showcase a Healthier Home

Use Plants to Showcase a Healthier Home New 3 World Trade Center to mark another step in NYC's downtown revival

New 3 World Trade Center to mark another step in NYC's downtown revival Why don’t potential homebuyers shop around for their mortgage?

Why don’t potential homebuyers shop around for their mortgage? Candy makers at Disneyland Resort are already planning the 2019 holiday sweets, including the famous hand-pulled candy canes

Candy makers at Disneyland Resort are already planning the 2019 holiday sweets, including the famous hand-pulled candy canes