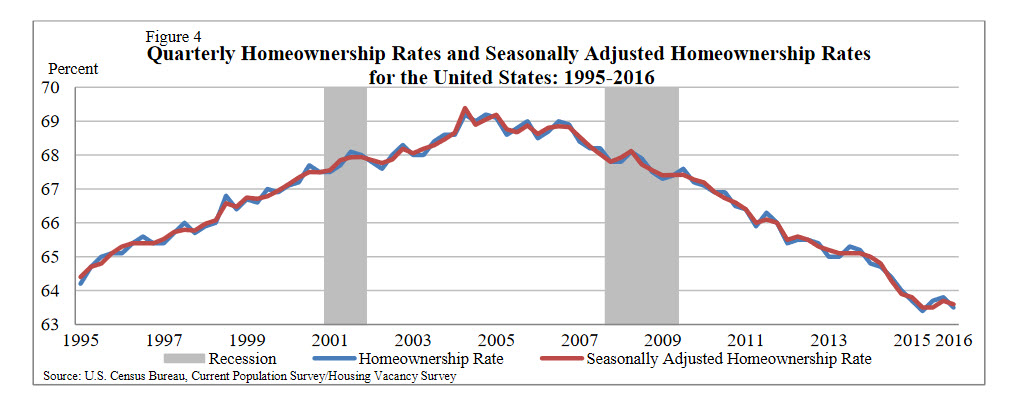

The national homeownership rate has just fallen to its lowest level since June 1965, the month that the Rolling Stones released “I Can’t Get No Satisfaction” and Peter Sellers and Romy Schneider starred in “What’s New Pussycat”. Only 62.9 percent of families now own the homes in which they live.[1]

“They’ said homeownership wouldn’t get any lower because the largest generation in history, the Millennials, was growing up and getting ready to buy their first homes. “They” declared both 2013 and 2014 to be the “Year of the Millennials.” When that didn’t happen, “they” said it would only be a matter of time before Millennials usher in the next golden age of real estate.

Well, looks like “they” were wrong.

f you own a home or make a living buying and selling real estate, you’ve got good reasons to be concerned that homeownership not only won’t recover but could keep on sinking back to the levels of the early 1960s, when Psycho was released, and Roy Orbison recorded “Only the Lonely”.

The truth is that over the past few years, Millennials have been withdrawing from homeownership, not embracing it. Some hard data:

- Four years into the housing recovery, the homeownership rate for owners younger than 35 has fallen to 34.1 percent, the lowest level since 1994[2]. That’s just over half the national homeownership rate. Buyers aged 25 to 34 accounted for only 28 percent of home buyers last year, down from 30 percent in 2006.[3] The share of first-time home buyers, who play a critical role in driving demand in local real estate markets, declined from 50 percent in 2010 to around 32 percent so far in 2016– the lowest since 1987.[4]

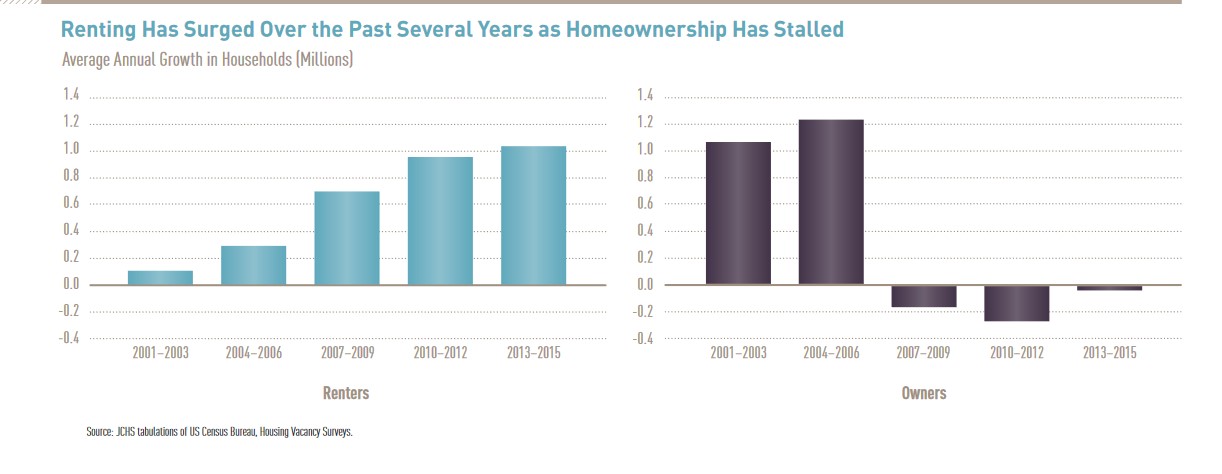

- Through the second quarter, renters occupied about 36.3 percent of households last year, the highest figure in a decade.[5] As Millennial homeownership declined over the past decade, the number of renter households under 30 years old rose from 10 million to 11 million, representing about 11 percent of renter growth in 2005–2015.[6]

How could this happen? Survey after survey shows that most Millennials really want to own homes. Employment and income levels are steadily improving. Interest rates have been ridiculously low for several years. Mortgages are more available today than they have been since the boom a decade ago. Lending standards are looser and low down payment options abound. Millennial buyers are better educated about the process and better qualified than their parents or older siblings when they apply. Virtually any young household with decent credit, two earners and a little cash can buy a home.

Five reasons why rentals are winning the battle for Millennials:

- Homeownership has become the victim of its own success.

Most homeowners are happy with the recovery to date, but they certainly aren’t hoping it will slow down. Since median national home prices hit bottom in February 2012 in Case Shiller’s national index, prices through June have risen 40 percent, an extraordinary recovery by any measure. But if you bought at the peak in 2006, you could still be 6 percent in the red. [7] In fact, some 4 million homes, or 8 percent of all homes with a mortgage, are still under water and 9.1 million, or 18 percent, still don’t have enough equity to refinance or sell.[8] Even owners who are back in the black lost nearly a decade of appreciation.

For young buyers, the price recovery is a nightmare. After rising an average of 10 percent annually over the past four years, median increases now are rising 4-5 percent annually. Their incomes aren’t rising anywhere near those rates. Moreover, prices are rising twice as fast for “affordable” price tiers. Perhaps the cruelest irony is that in the handful of markets where Millennial incomes are highest—New York, San Francisco, Seattle, Boston, Los Angeles, Chicago—home prices are highest and rising even faster.

- 2. Mysterious inventory shortages artificially inflate prices.

Perhaps NAR’s Lawrence Yun put it best when reporting a sudden drop in July sales. “Severely restrained inventory and the tightening grip it’s putting on affordability is the primary culprit for the considerable sales slump throughout much of the country last month,” he said. “Realtors are reporting diminished buyer traffic because of the scarce number of affordable homes on the market, and the lack of supply is stifling the efforts of many prospective buyers attempting to purchase while mortgage rates hover at historical lows.”[9]

Sales are slacking off for the balance of this year, yet prices are still hot. CoreLogic forecasts that home prices will increase by 5.4 percent on a year-over-year basis from July 2016 to July 2017. Prices are rising so much faster than incomes in hotter markets, that they are setting off “bubble alarms”.

A perfect storm of disparate factors is causing the inventory drought. Years of depressed new home construction has devastated new home inventories and battered home builders have taken years to regain production capacity. The lingering effects of the bubble and bust have kept equity-challenged owners from selling. Some nine million homes—many former foreclosures that were inexpensive starter homes—have been removed from the ownership inventory and converted to rental. That’s nearly twice as many homes as Americans buy every year. Add to the list millions of prospective move-up buyers who can’t sell until they can find a new home that they can afford and too many Boomers who would rather “age in place” than sell the family home.

- 3. Debt is eating young adults alive.

The price young adults are paying for college is well known. Some 43.3 million Americans with student loan debt, most of whom are under 40, have student loan debt. The average monthly student loan payment (for borrower aged 20 to 30 years) is $351.[10]

Many Millennials are added their student loan debt burdens with consumer debt. According to research Gallup research, more than third of Millennials say they don’t have enough money to live comfortably, and many of those appear to be using their credit cards to supplement their available resources with high-interest credit. Some 60 percent of Millennials making less than %48,000 a year enjoy spending money and most of them more carry more credit card debt (58% more), more student loan debt (23% more), more auto loan debt (26% more) and more personal loan debt (18% more) than millennials who prefer saving.[11]

- 4. Millennials will find it easier to stay put as rents are flattening faster than home prices.

It takes time to finance, site and build new apartments, but over past five years, apartment construction has been operating on overdrive to meet the Millennial demand. With more than 240,000 units expected to deliver across the top 54 U.S. markets this year, CoStar projects 2016 to be the peak year in the current cycle for new apartment construction. More than a half a million additional units are under way across the country, nearly twice the historical average since 1982. [12]

The new capacity is already being felt. Apartment rental rates are actually declining so much in several of the nation’s hottest major real estate markets that the national annual effective rent growth rate fell to 3.1 percent in July, which recorded the lowest rate since 2.8 percent in July 2014, according to the latest report from Axiometrics. Houston’s 2.2% annual effective rent growth in July marked the fourth straight month the metro was below zero; San Francisco saw apartment rents fall 1.21 percentage points to -0.7%, the first time the market was negative since April 2010; New York City posted a -0.2% annual effective rent growth in July, the first time it was in negative territory since January 2014.

As more units enter market across the nation in markets where demand has not been as strong over the next two years, look for rents to flatten and decrease. Most experts predict home prices will also cool,[13] but rents are now rising slower than existing homes and are flattening out faster than home prices. More importantly, rents in the hottest markets for Millennials are falling faster as capacity grows while inventories of affordable homes in those markets show no sign of increasing any time soon.

- 5. Single family rentals provide a new option for Millennial households.

No longer do young families have to buy a home to enjoy more space, a sense of community and many of the benefits of homeownership: good schools, security and a sense of community.

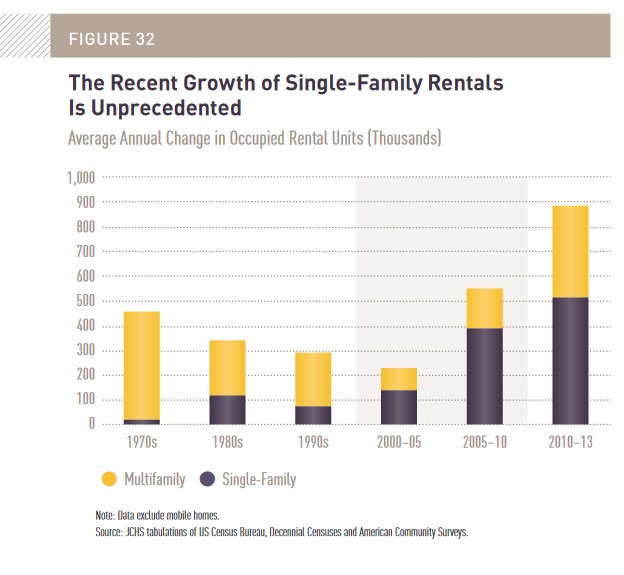

Today more than 15 million households and over 47.6 million people—about 43 percent of all renters—live in single family rentals.[14] In a matter of weeks. Millennials households move into a single family rental in a neighborhood where they could not afford to buy. These are more likely to be located in the central city and inner suburban markets than apartments. More than 40 percent of single-family rentals are located , and a third are in central cities. They actually account for a slightly larger share (27 percent) of the rental stock in central cities than units in large multifamily buildings with 20 or more units. Price-wise, single family homes serve a wide range of the market, accounting for 37 percent of all unassisted units renting for less than $400 a month, but also having among the highest median rents of any other rental category.[15]

[1] http://www.census.gov/housing/hvs/files/currenthvspress.pdf

[2] http://www.census.gov/housing/hvs/files/currenthvspress.pdf

[3] National Association of Realtors, Profile of Home Buyers and Sellers, 2006 and 2015. National Association of Realtors, Existing Home Sales 2016.

[4] National Association of Realtors 2015 Profile of Home Buyers and Sellers

[5] http://www.census.gov/housing/hvs/files/currenthvspress.pdf

[6] ww.jchs.harvard.edu/sites/jchs.harvard.edu/files/ch_1_rental_housing_demand_from_americas_rental_housing_2015_web.pdf

[7] https://www.spice-indices.com/idpfiles/spice-assets/resources/public/documents/395144_cshomeprice-release-0830.pdf?force_download=true

[9] http://www.realtor.org/news-releases/2016/08/existing-home-sales-lose-steam-in-july

[10] https://studentloanhero.com/student-loan-debt-statistics-2016/

[11] http://www.gallup.com/businessjournal/189713/americans-buried-mountain-debt.aspx

[12] http://www.costar.com/News/Article/Apartment-Construction-Hits-Peak-Year-as-Rents-Occupancies-Edge-Higher/182165

[14] http://www.nmhc.org/Content.aspx?id=4708

[15] w.jchs.harvard.edu/sites/jchs.harvard.edu/files/ch_2_rental_housing_supply_from_americas_rental_housing_2015_web.pdf

Related Posts

A.J. Pollock, Russell Martin hit home runs in Dodgers’ loss to Indians

A.J. Pollock, Russell Martin hit home runs in Dodgers’ loss to IndiansCalifornia had 77 of the country's 100 most expensive ZIP Codes for home sales last year, report says

The Latest in Tile Trends From Coverings 2018 (22 photos)

The Latest in Tile Trends From Coverings 2018 (22 photos) 8 Elements for a ‘Crazy Rich Asians’-Style Home (9 photos)

8 Elements for a ‘Crazy Rich Asians’-Style Home (9 photos) Extended cut: Sorkin interviews Buffett on the 2008 financial crisis

Extended cut: Sorkin interviews Buffett on the 2008 financial crisis Billionaire Ron Burkle chases record $29 million for Bob Hope's Toluca Lake estate

Billionaire Ron Burkle chases record $29 million for Bob Hope's Toluca Lake estate